Welcome back!

Scene One – Providing Entity

Hi Alan and Rose! Winnie here from Quill Group Financial Planners, presenting to you your personalised video Statement of Advice today. My authorising licensee and contact details are on the screen now, should you wish to reach out to me at any time. Okay, lets get right into it.

Same as all Scene 1

Scene Two – The Client

Retired, independent children,

Allan and Rose, you are retirees age 78 and 76 respectively. You recently helped your daughter financially with funds from your overdraft facility. You are seeking our help with using your superannuation to pay down the overdraft and help meet your retirement costs.

You are both in your 70s and are retired, with independent children. You recently provided financial help to your daughter with funds from your overdraft facility. You are seeking advice on using your superannuation to pay down the overdraft and meet your retirement costs.

Show 70yo man and woman on a beach sitting on chairs, top left, then show same couple with one adult male child and one adult female child next to them, top right. Then on the same image, show a arrow going from the parents to the daughter, and label it with a dollar sign. Then on bottom left, show superannuation building with bank building next to it, and arrow going from superannuation building to bank building labelled with a dollar sign. Then on bottom right, show image of cash notes and coins

Scene Three – Scope And Goals

• Retirement income– you wish to have sufficient income to meet your annual living expenses of $57,885.

• Debt management – you would like to get rid of your overdraft of $47,250 as soon as possible.

• Centrelink entitlements – you wish to access any entitlements available to you.

• Professional management– you are seeking guidance with managing your retirement savings.

• Estate planning– you wish to ensure estate planning documents reflect your current wishes.

We therefore agreed that this advice will cover superannuation platforms and underlying investments, as well as pensions. Your goals are to retire with an annual income of just under 60 thousand dollars, pay down the $47,250 overdraft as soon as possible, access any Centrelink benefits you may be eligible for, have your retirement assessts managed by professionals, and review your estate planning arrangements.

Scope:

1. Superannuation (platform)

2. Superannuation (investments)

3. Pension

Goals:

1. Maintain $57,885 in retirement

2. Pay down $47,250 ASAP

3. Centrelink benefits

4. Professional management of assets

5. Review estate planning

Scene Four – The Advice

Retirement Income Planning; Professional Management; greater investment choice, availability of independent research on investment options, access to unbundled tax structure, superior administration, includes a cash account to act as a hub for investment income and pension payments

performance cannot be guaranteed, costs will be higher

make a $30K Lump Sum Super Withdrawal from Allan’s account to paydown $22,250 of your $47,250 overdraft

Reduce debt and save interest (overdraft interest rate 9.73% per annum)

funds not available for retirement income

Use $7,750 remaining from the Lump Sum Super Withdrawal to set up a bank account for day to day use and to receive investment property income.

To separate your day to day banking from your overdraft. This will stop you from incurring interest charges on your daily spending.

Establish loan agreement with your daughter for $25,000 loan. Include agreement to pay interest and overdraft fees to you monthly. Based on current interest of 9.73% per annum, interest costs are around $203/month in addition to overdraft fees are $14/month.

Formalise loan arrangements and help your daughter recognise costs involved with the lending.

Start Account Based Pension with minimum pension payments

Ongoing tax free retirement income to meet retirement needs.

You may outlive your pension funds, depending on investment returns and drawdown rate

Apply for Commonwealth Seniors Health Care Card

Receive discounted rate on medicines listed on Pharmaceutical Benefits Scheme, Bulk Billing for doctors’ appointments, discounted out-of-hospital medical expenses above the concessional threshold of the Medicare Safety Net

Review Estate Plan

Estate planning documents to reflect your current wishes.

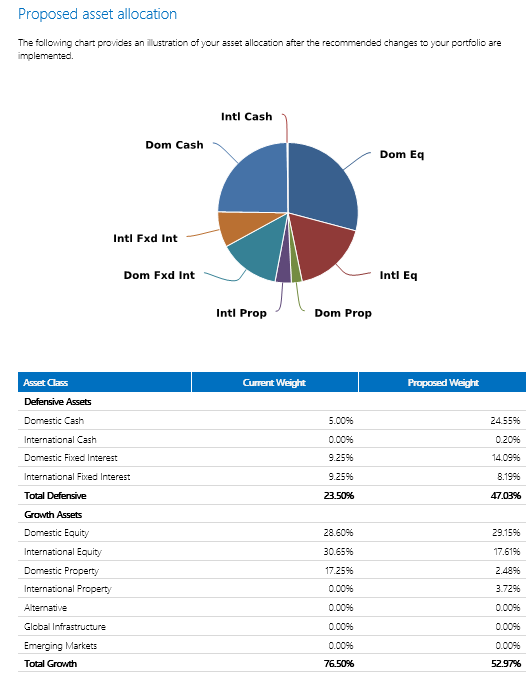

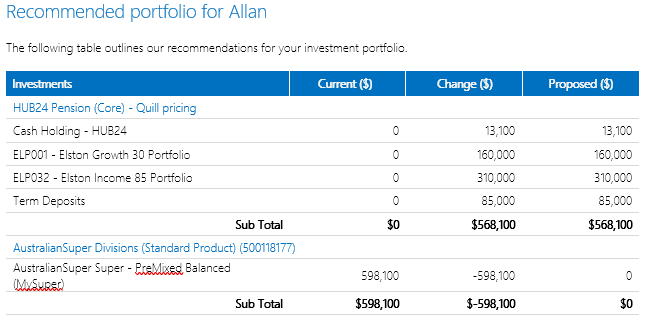

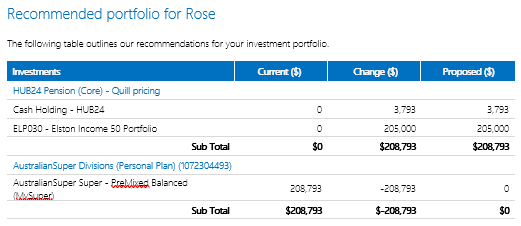

Allan and Rose to use HUB24 Super/Pension (Core Menu) as the destination account for existing Australiansuper accounts. Dollar Cost Averaging? Yes, over 5 months into proposed super/pension investments (excluding term deposits) ALLAN: Cash $13100 Elston Income 85 SMA $310K Elston Growth 30 SMA $160K Term Deposit $85K ROSE: Cash $3K Elston Income 50 SMA $205K

Proposed product provides access to SMAs to help keep portfolio aligned to your BALANCED risk profile, visibility on investments, ability to in specie transfer investments, speedier processing via adviser transacting and a cash account to act as a hub for investment income and pension payments. Also offers unbundled tax structure and non-lapsing binding nominations.

performance cannot be guaranteed, costs will be higher

My first advice is for you both to rollover your fund balances from your existing Australian Super funds to HUB24 Super, Core Menu and invest the funds into the following investments across the span of five months - a strategy known as dollar cost averaging. This will unlock greater investment options, access to unbundled tax structures, better administration, will include a cash account to act as a hub for investment income and pension payments, and will be professionally managed. Please note however, that investment performance cannot be guaranteed, and your costs will also be higher due to the additional features.

My second advice is for Alan to make a $30,000 lump sum withdrawal to pay down $22,250 of the overdraft. This will enable you to reduce debt and avoid interest being paid at 9.73% per annum, although it does mean that you will have less funds available for retirement.

My third advice is to use the remaining $7,750 from your lump sum withdrawal to set up a bank account for day to day use and to receive investment property income. You will benefit by separating your day to day banking from your overdraft and will therefore avoid incurring interest charges on your daily spending.

My fourth advice is to establish an arrangement with your daughter for the remaining $25,000 loan. Include an agreement to pay interest and overdraft fees to you monthly, which would be interest costs of $203 a month at the 9.73% per annum rate, and overdraft fees of $14 per month. Formalising such an agreement will help your daughter recognise and appreciate the costs involved with lending.

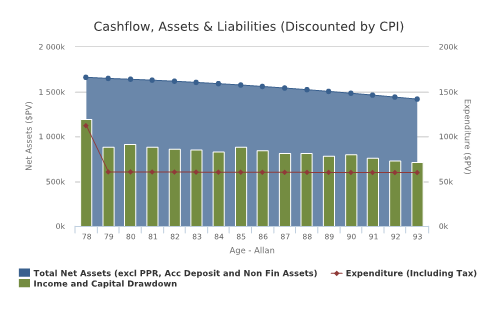

My fifth advice is for both of you to commence an account based pension with minimum pension payments, initially amounting to $34,090 for Alan in the first year and $12,530 for Rose in the first year. This would result in ongoing tax-free retirement income to meet your retirement needs. Please note that you may outlive your pension funds, depending on the investment returns and drawdown rate.

My sixth advice is for you both to apply for the Commonwealth Seniors Healthcare Card. Holding this card enables you to receive discounted rates on medicines listed on the Pharmaceutical Benefits Scheme, bulk billing for doctors appointments, and discounted out-of-hospital medical expenses above the concessional threshold of the Medicare Safety Net.

My final advice is that we should organise a meeting with appropriate legal professionals that can advise you on your estate planning and power of attorney requirements. This is important so that your estate planning documents reflect your current wishes and I am happy to facilitate this meeting.

Advice 1 - same as previous rollover for husband and wife, existing building label Australian Super logo, new building label HUB24 logo. Green tick: Greater investment options, Unbundled tax structure, Ease of administration, Included cash account, Professionally managed. Red exclamation: Investment performance is not guaranteed, Fees higher than existing fund.

Advice 2 - show image of Alan, then building with Aus Super logo, then blue arrow labelled $22,750 / $30,000 and then pointing to bank building labelled "Overdraft". Green tick: Reduce debt, Avoid 9.73% interest. Red exclamation: Less funds for retirement.

Advice 3 - show same as above, but blue label is $7,750 / $30,000 and image after blue arrow will be bank building with label "Daily Account". Green tick: Avoid interest on daily spending

Advice 4 - showimage of daughter on left, image of paper contract with pen in middle with label Loan Agreement, and image of husband wife on the right. Above the contract image, include label "Interest costs: +$203pm" and under that label "Overdraft fees: +$14pm". Green tick: Daughter will be better informed and will appreciate finances

Advice 5 - show image of Alan, then super building with HUB24 logo, then nest, then label "$34,090 Y1 pension". Then show same thing in next row for Rose, but label "$12,530 Y1 pension". Then on bottom green tick: Ongoing tax free retirement income, Meets retirement needs. Red exclamation: May outlive pension funds.

Advice 6 - show image of Seniors Card like previous video. No other image, so make it big. Green tick: Discounted medicine, Bulk billing, Discounted medical expenses

Advice 7 - show image of one woman and two men having a meeting at a table. Green tick: Your estate treated as per your wishes.

Scene Five – Fees And Costs

Product fees

Projection.png

{kind=link}

allan-asset-alloc.png

{kind=link}

allan-portfolio.png

{kind=link}

allan-product-costs.png

{kind=link}

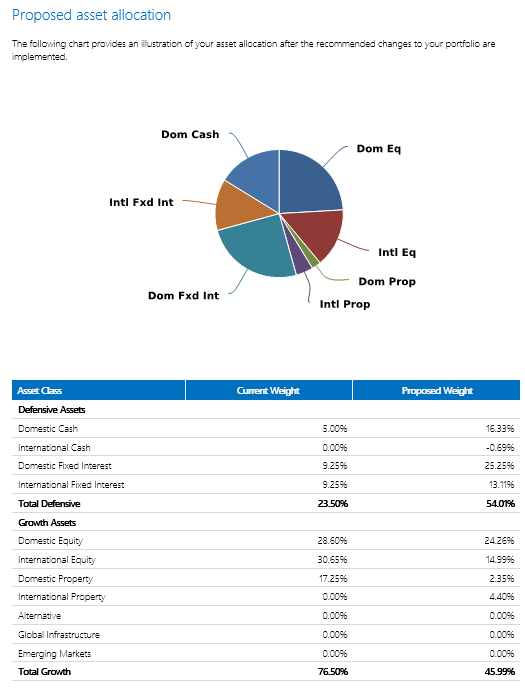

rose-asset-alloc.png

{kind=link}

rose-portfolio.png

{kind=link}

rose-product-costs.png

{kind=link}

Let's discuss fees. There are three categories of fees that you need to be aware of

The first is a one-off advice fee of $4,235 which covers the research, formulation and implementation of this advice.

Next, there is an ongoing fee, which amounts to $6,490 per annum, of which $4,730 is deducted from Alan's super fund and $1,760 is deducted from Rose's super fund. This ongoing service fee places you on our Essentials Package, which means you will receive the following services annually

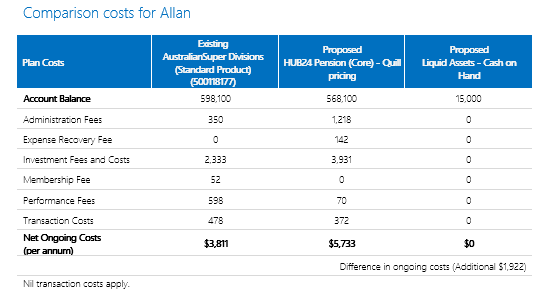

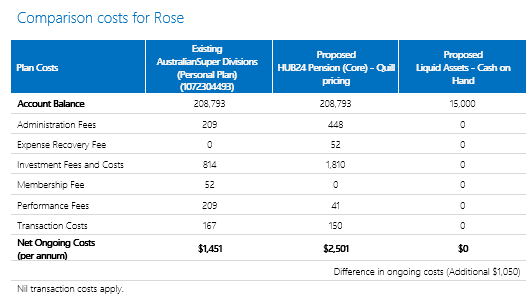

Lastly, please note the following two tables. The first demonstrates that Alan's product costs amount to $5,733. The second demonstrates that Rose's product costs amount to $2,501.

Same as previous videos with "Essentials" package

Scene Six – Disclosures

We have now covered the advice in full and with that, there are a few important points I need to make.

This Statement of Advice is for your consideration and your use only.

We have based this advice on information gathered from our discussions, and your completed Client Confidential Data Collection Booklet. We have assumed that this information is correct. Should any information have changed or be incorrect, you should contact us so we can review these strategies.

For information regarding benefits, interest and associations, please refer to the Financial Services Guide. We have already provided a copy, however you can view the latest version on our website. Alternatively we can e-mail or post a copy to you on request.

After you acquire certain financial products, a 14 or 28 day cooling off period will apply in certain circumstances. This means you can cancel or transfer to another financial product within this period if you decide this financial product no longer meets your needs. Please refer to the relevant product disclosure statement for details regarding your cooling off rights.

Finally, my advice remains current for a period of 30 days from the date of this video. If you decide to implement our recommendations after this time, or if your circumstances change during this time, please contact me so we can confirm that the advice continues to be suitable for you.

This advice purely considers your interests only, and is in your best interests. Please sign the authority to proceed if you wish to proceed with my advice. Otherwise, if you have any questions, please let me know. Thank you!

1. This SoA is for you only.

2. Let us know of any incomplete or inaccurate information immediately.

3. While we do not share any association with any of the products we have recommended in this advice, please refer to our FSG for further disclosures on any broad associations we may have.

4. 14-28 day cooling off period - please check relevant PDS

5. This advice is valid for 30 days from today's date.

Rest of scene is same as other final scenes