Welcome back!

Scene One – Providing Entity

Hi Veronica! Roger here from Smart Start Financial Services, presenting your personalised video Statement of Advice today. My authorising licensee and contact details are on the screen now, should you wish to reach out to me at any time. Okay, lets get right into it.

Same as all Scene 1

Scene Two – The Client

Employment contract lawyer

You have just purchased an off the plan investment property. I would like to review our current superannuation to ensure our investments are appropriately aligned with our risk profile. To have a superannuation structure that provides greater investment flexibility, transparency, and control to help achieve stronger long-term outcomes aligned with our retirement objectives. I wish to maximise my income protection insurance to cover my full salary and to possibly hold this insurance in super to ease maintain adequate cash flow. I wish to have enough insurance cover, particularly life cover to manage debts. I want financial advice and an ongoing working relationship with a financial adviser

You are 36, are working as an employment contract lawyer and have just purchased an off-the-plan investment property. You have come to me to seek financial advice and to also have an ongoing working relationship with a financial adviser.

Show Alice as a young 30yo ASIAN girl in a business suit, then show a picture of a house with a sign in front saying "SOLD". Then show photo of Alice again, shaking hands with a Caucasian 50yo man in a suit also.

Scene Three – Scope And Goals

Consult with a financial adviser to ensure that I am in a better financial position.

I wish to maximise my income protection insurance to cover my full salary and to possibly hold this insurance in super to ease maintain adequate cash flow.

I wish to have enough insurance cover, particularly life cover to manage debts.

I would like to review our current superannuation to ensure our investments are appropriately aligned with our risk profile. To have a superannuation structure that provides greater investment flexibility, transparency, and control to help achieve stronger long-term outcomes aligned with our retirement objectives

I wish to potentially move to a larger property and either rent or sell my current residence.

I want financial advice and an ongoing working relationship with a financial adviser

We agreed that this advice will cover insurance, superannuation platforms, and underlying investments. Your first goal is to maximise your income protection to cover your salary and hold this insurance within super to ease cashflow. Your second goal is to have sufficient insurance cover, particularly life cover to manage debts. Your third goal is to review your current superannuation to ensure it is aligned with your investment risk profile. You also wish to have a superannuation structure that provides greater investment flexibility, transparency and control to help achieve stronger outcomes in retirement.

Scope:

1. Insurance

2. Superannuation (platform)

3. Superannuation (investments)

Goals:

1. Maximise income protection insurance, hold in super

2. Sufficient insurance cover, in particular life insurance

3. Review super investments to ensure alignment with risk profile

4. Review super product and obtain greater investment flexibility, transparency and control

Scene Four – The Advice

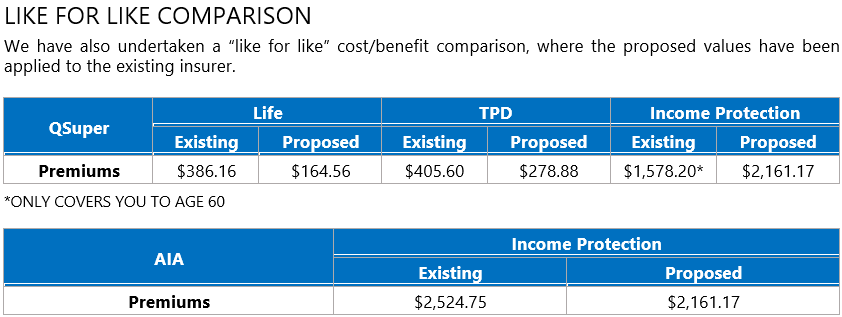

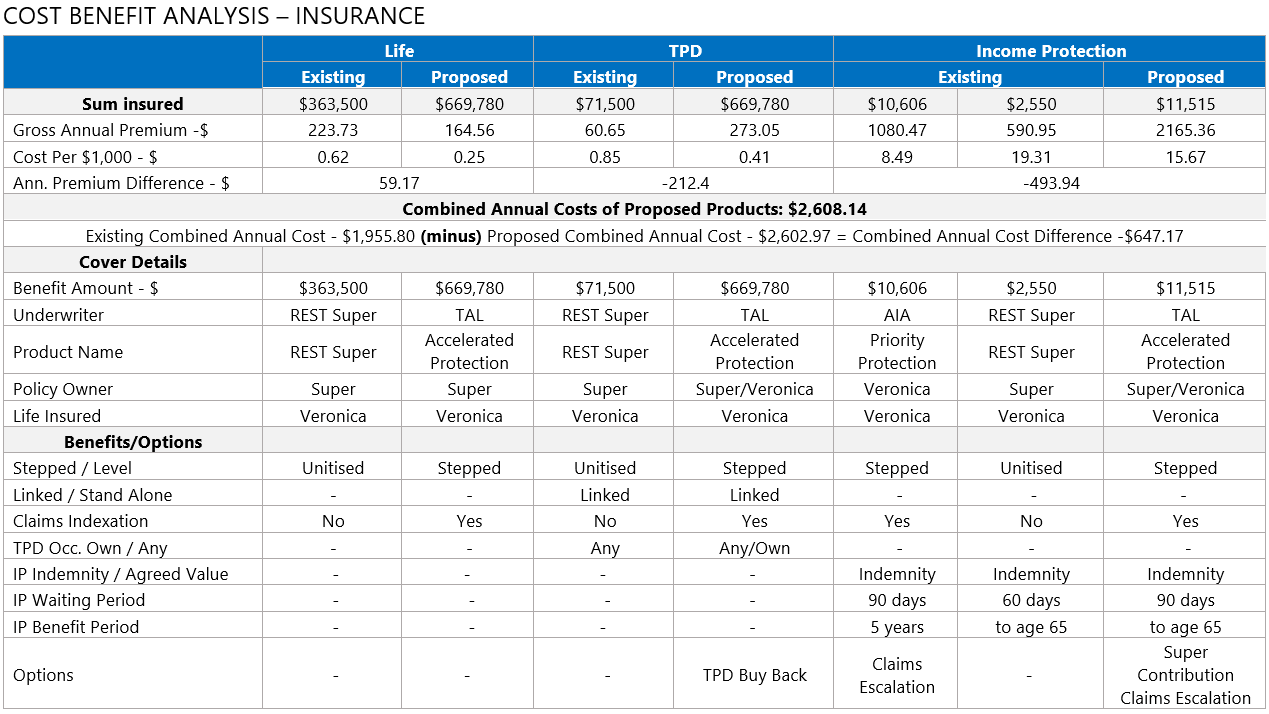

• We are recommending moving from unitised insurance cover within your super fund to a retail insurance policy, as retail cover provides more comprehensive and customisable benefits, including fixed levels of cover, offering greater certainty and long-term cost efficiency. • The recommended structure balances cost-efficiency, comprehensive protection, and access to benefits, ensuring you are adequately covered without placing undue strain on her personal finances. • Life insurance pays a lump sum if you pass away or meet the terminal illness requirement, to help cover expenses and/or provide ongoing income for your family. TPD insurance pays a lump sum if you meet the policy definition of permanently disabled and are unable to ever work again. • Trauma (or Critical Illness) cover is designed to pay you a lump sum in the event that you suffer a specific illness or injury, such as heart attack or stroke, that may not leave you disabled long term but is traumatic at the time of occurrence. Treatment and recovery can be life-changing and costly. • Income protection cover will replace a large percentage of your income if you are unable to work for a period of time due to illness or injury to protect your lifestyle. • We recommended that your Life and the TPD (Any Occupation) portion cover be held inside superannuation to reduce the impact on your personal cash flow, as premiums are funded from your super balance. Additionally, you may be eligible to claim a 15% tax rebate on premiums, further enhancing the cost-effectiveness of this structure. • The Own Occupation TPD benefit is structured outside super under a split policy arrangement, ensuring you maintain tax-free access to benefits in the event of a claim without needing to meet a superannuation condition of release. We have recommended this structure to provide you with a higher quality of cover, as your existing policy does not include Own Occupation. This ensures an upgrade in benefit terms as part of the restructure. Own Occupation TPD is particularly valuable for your profession as a Solicitor, as it allows you to claim if you are permanently unable to work in your specific medical specialty, even if you are capable of working in another field. This provides more tailored protection aligned with your specialised skills and income level. • We recommend holding your Life, Total & Permanent Disability (TPD) and a portion of your income protection cover inside superannuation to reduce the impact on your personal cash flow, as premiums are funded from your super balance. Additionally, you may be eligible to claim a 15% tax rebate on premiums, further enhancing the cost-effectiveness of this structure. • We recommend holding your Income Protection cover outside of superannuation to ensure access to more comprehensive policy features, including a wider range of ancillary benefits, and to avoid potential claim delays or restrictions related to superannuation conditions of release. Additionally, premiums paid personally are generally tax-deductible, providing further financial benefit. Reasons for recommendations and how our advice meets your objectives • TAL was one of the few insurers willing to offer Income Protection cover below $1,500 per month, ensuring suitable protection aligned with your current income level. • Premiums are cost-effective compared with other providers offering similar policy terms, making the cover affordable while maintaining adequate benefits. • Flexible policy options, including split ownership (inside and outside super) and multiple waiting/benefit periods, allow the policy to be tailored to your cash-flow and coverage needs. • TAL provides comprehensive definitions and ancillary benefits (such as rehabilitation and specified injury benefits) that enhance claim flexibility and value. Features • Linked TPD and Trauma insurance will be linked to your life cover. This helps to reduce the premiums payable but causes the life cover to be reduced by the amount of a TPD or Trauma claim. • TPD insurance has been “split” between superannuation and personal ownership, allowing most of the premium to be funded from superannuation while still retaining an “own occupation” definition outside of super. Own occupation means you are considered totally and permanently disabled if you cannot perform the specific job you are trained and experienced in, whereas any occupation (the stricter definition required inside super) means you must be unable to perform any job you are reasonably suited to by education, training or experience. Splitting the cover gives you the tax-effective funding benefits of super while keeping the stronger and more flexible own-occupation definition for claims • Trauma Reinstatement - Trauma reinstatement provides the option to reinstate up to 100% of the trauma cover, 12 months after a trauma benefit has been paid, without underwriting. Medical conditions related to the original claim will be excluded. This means that you will be eligible to claim on your policies more than once for different illnesses. • Indemnity: An indemnity income protection contract allows the insurer to reduce your monthly benefit based on your historical income at the time of claim. This cover is typically lower cost and is suitable for cover held entirely within a superannuation environment. • A 90-day waiting period is recommended for Income Protection cover, as the clients maintain a sufficient cash buffer and accessible savings to meet living expenses during this timeframe. This allows them to reduce premium costs while still ensuring income protection for longer-term illnesses or injuries, without compromising their financial security in the short term. • A “to age 65” benefit period has been selected so that you can receive income protection payments for the long term if required. • As this cover is only expected to be required in the short to medium term (until your debt is extinguished) we expect that stepped premiums will be the most cost-effective option for you over the life of the cover. • TPD and Trauma Buy-Back – If a TPD or Trauma benefit is paid, you can repurchase Life cover up to the amount of the benefit paid without the need to supply further medical evidence. This feature helps restore your Life insurance following a claim, ensuring continued protection for your beneficiaries. We believe you will be better off if you switch from your existing product, namely REST Super, to our proposed product namely TAL because: • Your existing insurance is based on a unitised structure for both premiums and sum insured. Under this structure, not only do premiums increase with age, but the level of cover also decreases over time — potentially leaving you underinsured in the future. By switching to a stepped premium structure with a fixed sum insured, we can ensure your cover remains appropriate and aligned with your ongoing needs, while providing greater control and certainty over the level of protection in place. • Your new level of recommended cover correctly reflects our understanding of your current financial situation. • The policy does automatically increase the sum insured in line with indexation. • The policy will continue to be renewed under the same terms and conditions regardless of any changes to the Insured's health, occupation or pastimes. • Indexation continues until the policy expires. • Provided premiums are paid on time, the underwriter cannot terminate the policy prior to the expiry date. • Splitting TPD cover between super and personal ownership provides greater flexibility and claims certainty — the super-held portion satisfies SIS conditions, while the personally-held portion avoids super release restrictions, giving stronger definitions, faster access to benefits, and reduced risk of a claim being delayed or rejected due to preservation rules. • Holding Income Protection under a split structure allows premiums to be funded through both super and personal cashflow, reducing superannuation erosion while ensuring the policy retains stronger, more comprehensive definitions outside super, and enabling claims to be paid without reliance on superannuation release conditions. • You will gain $8,965 / m of Income Protection cover with a benefit period to age 65. • You will gain $306,280 more in Life cover and $598,280 in TPD cover.

• Insurance benefits such as Life, TPD (Any Occupation), and a portion of Income Protection held inside superannuation are subject to superannuation conditions of release. This may delay or restrict access to funds, particularly in situations where the insured event does not meet a condition under superannuation law. • Depending on how benefits are paid (e.g. to non-dependants or via a lump sum from the super fund), tax may be payable on insurance proceeds held within super, whereas benefits paid from personally held policies are generally received tax-free. • A split ownership structure (with cover held both inside and outside super) introduces additional administrative complexity and requires ongoing monitoring to ensure premium funding remains aligned and benefits are not unintentionally lapsed or disrupted. • As Trauma insurance cannot be held within superannuation, the premiums must be fully funded from your personal after-tax income, which may affect your cash flow over time. • Replacing existing policies means you are moving to a new insurance product with current insurer terms, conditions, and underwriting requirements. These may differ from your previous cover and could affect eligibility or claim outcomes. • By cancelling your existing policies, you may forfeit older policy benefits, pricing structures, or definitions no longer available in the market. Although we have sourced comparable cover, some differences may still apply. • If benefits are paid from superannuation to a non-tax dependant, such as an adult child, a portion of the benefit may be subject to tax, reducing the net payout to beneficiaries. • As policies are newly underwritten, you may be subject to medical or occupational exclusions or loadings that could affect future claim eligibility. These will be confirmed upon completion of underwriting. • All recommendations are based on current legislation. It is possible that future changes in government policy and legislation may have a negative effect on the recommendations made in this plan. • The proposed insurance cover will have an impact on your superannuation. o By funding your PPS Mutual insurance through super your balance, according to our projections, after 10 years your super will be $5,911 lower than if you paid for the premiums directly. This gap will widen in the years ahead if you choose not to contribute additional funds into your superannuation balance to offset these insurance costs. Please refer to the table below. • Stepped premiums increase every year with age and will become expensive as you get older. • Your insurance does not commence until the insurer has completed their assessment, approved your application and issued the insurance policy. • Life insurance products have a cooling-off period during which you can check that it meets your needs. Within this period, you can cancel the cover. Details about the cooling-off period are set out in the Product Disclosure Statement. • When completing your insurance application, you have a duty to disclosure relevant information that may affect whether the insurer will agree to cover you. This includes personal information regarding your health, past times, and/or finances. The law expects you to disclose what a reasonable person in the circumstances could be expected to know is relevant. A good guide is the information set out in the application form. • Over time, your circumstances and need for insurance can change. It is important to regularly review your insurance arrangements with us to ensure you have the right cover in place to protect you and your family. • No death benefit will be paid in the event of death by suicide in the 13 month period from the date the life new insurance cover commences. • Once the insurer has received your application, they will advise what other requirements they have of you. This can involve having a blood test or a medical examination or they may write to your doctor for a report. We will let you know what these requirements are as soon as we have been informed. • For 3 years you will not be protected against non-fraudulent misrepresentation under the Insurance Contracts Review Act 1984 (CTH). You will need to ensure you have the recommended policy for at least 3 years to regain this benefit. In the event of fraudulent disclosure, a policy can be cancelled to inception. • Until your new insurance policy is in place and you have cancelled your current insurance, you could be paying some fees and charges twice - once for your current policy and once for your new policy. • If your health has changed since you took out your current policy, there may be more restrictions and/or exclusions in your new policy. You may also have to pay higher premiums. • For a Total and Permanent Disability claim to be paid, the diagnosis must meet the policy definition of the permanent disability. • When claiming on TPD, you will always be assessed under the 'Any Occupation' definition first and if you are unable to meet the conditions of release you will then be assessed under the 'Own Occupation'. • ‘Any’ occupation TPD definition, there may be a risk that you do not meet the requirements for a payout. • Your total and permanent disability insurance policy will require you to be totally unable to work for a period (usually three or six months) before the insurer has sufficient evidence that you will be unable to work again. • If you are under age 60, total and permanent disability payments from superannuation will be taxed when paid to you. For details of what tax may apply to you, talk to your tax adviser. • With an ‘indemnity’ contract, proof of income will be required in the event of a claim. If your income is lower than normal in the period prior to claim then your monthly benefit may be less. • Under an indemnity income protection contract an insurer can reduce your monthly benefit if your historical earnings at the time of claim are lower than the income that has been insured. • Income protection benefits are considered taxable income and taxed accordingly. • There is a 90 day waiting period before income protection benefits are payable, after which your benefit will be paid a further 30 days in arrears. • Income protection is only payable until age 65. • You should be aware that if you do not fully disclose all relevant and material information to the insurer as required, the insurer may be entitled to reduce their liability under your insurance contract in respect of a claim, or cancel your contract. • Not all medical conditions are covered by your insurance policy. Definitions of the specified medical conditions covered under the policy are listed in the PDS. • The additional policy features I have recommended are at an additional cost to you. • The premiums quoted may vary depending upon your family history, personal situation, personal statement provided, and underwriting assessments resulting in loadings and/or exclusions.

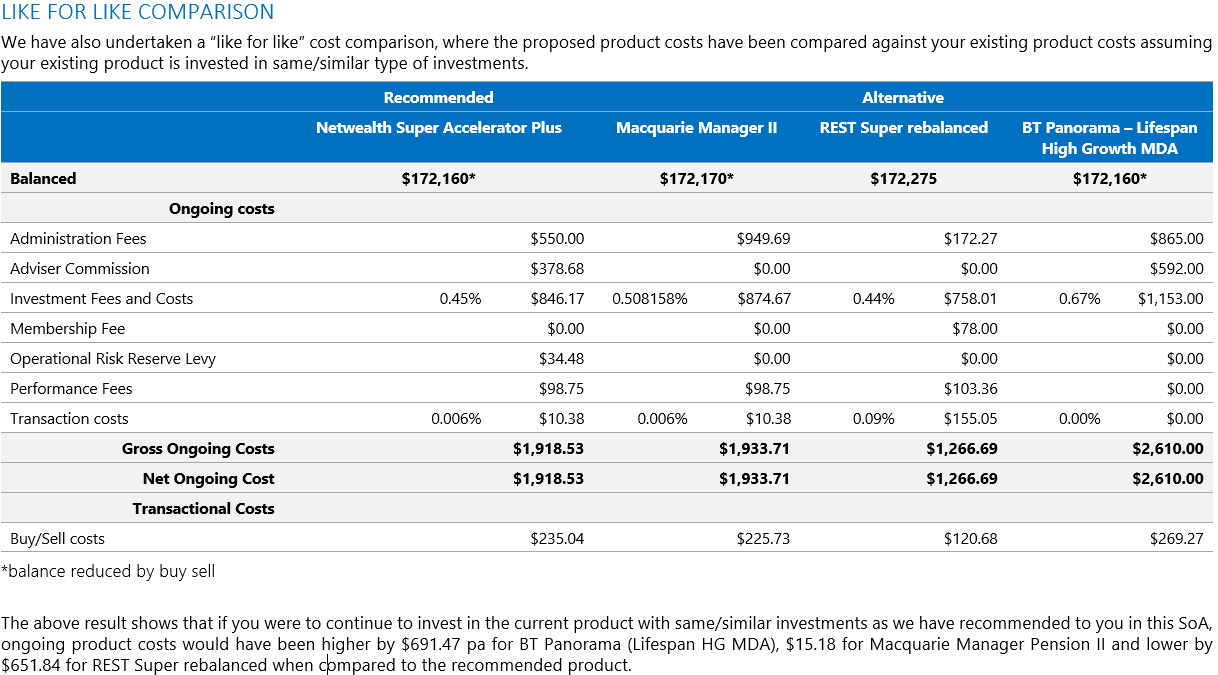

ROLLOVER YOUR EXISTING SUPERANNUATION FUNDS TO A NEW NETWEALTH SUPER ACCELERATOR PLUS FUND We recommend you rollover the full balance of you REST Super of approximately $172,126 to a new Netwealth Super Accelerator Plus Fund. Invest the funds into a OrionX High Growth Managed Discretionary Account (MDA) portfolio. Redirect your employer contributions to your new Netwealth Super Accelerator Plus Fund We recommend that you establish a binding non-lapsing death benefit nomination, to ensure your superannuation benefits are paid directly to her in accordance with your wishes and without trustee discretion.

• We recommend you rollover funds as the existing funds do not have the investment options which allow you to adopt the recommended portfolio construction strategy. • We will have greater transparency in your investments in the recommended product because we are able to not only pick the fund/s that you invest in, but we will also know which individual investments the fund manager will be investing the pooled funds in to on your behalf. In your current product, although we are able to choose a fund to place your superannuation monies into, we are not able to gain clear knowledge of all the individual investments that the fund manager is making with your funds, on your behalf. Having this level of transparency will help with developing your overall investment strategy, allowing us to achieve strong diversification and potentially increase your overall returns generated. This also gives you much more control in your investment choices. • The OrionX Managed Portfolio (MDA) has delivered competitive short-term performance compared to both REST Super, while providing enhanced diversification, transparency, and access to professional investment management. Some underlying investments within the OrionX portfolio are newer, and therefore do not yet have sufficient three- or five-year performance data. While this limits direct long-term comparison, it does not materially affect the portfolio’s overall risk and return characteristics. • Netwealth offers significant savings when one or more accounts from the same family group are held. The fee structure is ‘capped’ at a significantly lower level of overall funds under management than your existing superannuation platforms offer. This means cost savings achieved will increase each year funds are invested with Netwealth when compared to your existing. • Netwealth offers a tiered fee structure (that is also capped) the percentage fee will reduce over time as your funds grow in size from contributions and earnings, and hence become more competitive. • Netwealth offers a broader investment menu, including access to direct shares, ETFs, managed funds, term deposits, and access to our Managed Discretionary Portfolios, OrionX. This provides greater flexibility and control when constructing and managing a diversified portfolio. • The platform offers enhanced transparency with full fee and performance reporting, allowing you to easily monitor your investments and understand how your super is performing. • From a strategic standpoint, Netwealth supports seamless transition from accumulation to pension phase, meaning you can retain your chosen investments when you commence an income stream in retirement. • Any income paid from your investments will continue to be reinvested to benefit from compounding returns over the long term. • The Managed Discretionary Account (MDA) portfolio will be actively managed and rebalanced to maintain the target allocation across asset classes, consistent with your investment program and risk tolerance, while ensuring efficient exposure to both domestic and international markets. • As superannuation assets do not form part of your Estate assets, thereby are not covered in your Will, it is important that you make a death benefit nomination to ensure that your funds as dispersed as per your wishes.

• Your existing QSuper account will be closed following the rollover, and your current investment holdings will be sold down prior to transfer. This may result in realised capital gains or losses, which will be reflected in your super fund’s tax reporting. • Your overall ongoing fees will increase. • By proceeding with the recommended changes, you will lose any existing insurance cover held within your current superannuation fund. The recommended insurance within this Statement of Advice is intended to replace your existing cover. You should ensure the new cover is in place and meets your needs before the existing policy is cancelled. • All recommendations are based on current legislation. It is possible that future changes in government policy and legislation may have a negative effect on the recommendations made in this plan. • Market downturns may cause geared investors in margin lending plans to receive margin calls from their lenders. Gearing can also accelerate losses under adverse market conditions. • Your funds will continue to be in a preserved environment. There are restrictions as to when you can access the funds in superannuation. You will not be able to withdraw funds from superannuation until you meet a condition of release. • We have no control over financial markets and economic circumstances. Investments with inherent equity-based investments are volatile in nature as they are not capital guaranteed. The concept of volatility means that investment values can move both up and down. The greater the volatility the more ups and downs. The reward for accepting volatility is likely higher returns over the long term. • We cannot guarantee that by replacing your current superannuation fund, you will receive superior investment returns as opposed to an alternative fund. • You may incur buy/sell costs and other transaction costs when you sell existing investment and buy the recommended investment because of the rollover. • Your funds could perform poorly. Past performance is not necessarily indicative of future performance. • There is always a risk that the recommended investments will not perform as well as your current investments. • Your funds will spend some time out of the market in the rebalance process. • The exact amount transferred may change. This is because investments change in value daily. • If you made personal contributions to Superannuation and wish to claim a tax deduction for these contributions, you must lodge the request with the relevant Super product and receive an acknowledgment before implementing the recommended rollover.

Scene Five – Fees And Costs

Product fees

Super-comparison-table.png

{kind=link}

Insurance-comparison.png

{kind=link}

insurance-cost-benefit-analysis.png

{kind=link}

Let's discuss fees.

The first is a one-off advice fee of $1,350, which covers the research, formulation and implementation of this advice.

The second is an ongoing service fee of $1,000 per annum. This ongoing service fee will cover an annual review of your super portfolio and insurance suitability, monthly newsletters, and access to me as your financial adviser for adhoc financial discussions.

Same as previous videos.

Scene Six – Disclosures

We have now covered the advice in full. Please note that as the legislation, economic conditions and your own personal circumstances may change, the recommendations within this Statement of Advice expire two months from the date of issue. Once expired, confirmation of the information and recommendations within this Statement of Advice will be required before this material can be relied upon. Without such confirmation and further consultation, my licensee or I cannot support the recommendations that have been made. This advice purely considers your interests only, and is in your best interests. Please sign the authority to proceed if you wish to proceed with my advice. Otherwise, if you have any questions, please let me know. Thank you!

Same as all scene 6