Welcome back!

Scene One – Providing Entity

Hi Alice! Tony here from Quill Group Financial Planners, presenting to you your personalised video Statement of Advice today. My authorising licensee and contact details are on the screen now, should you wish to reach out to me at any time. Okay, lets get right into it.

Same as all Scene 1

Scene Two – The Client

Retired; Residing in a dementia care facility; care costs covered by existing income Financial decisions driven by best-interest duty and estate intent

Client represented by: Rachael & Erik Moore (Enduring Power of Attorneys) Rachael & Erik, you have engaged us to provide guidance on how best to manage the lump sum of surplus cash held in Alice’s name and to ensure her financial arrangements are aligned with her long-term needs and estate intentions. As it is unlikely that Alice will require the $410,000 in her bank account, the primary objective is to structure these funds for longer-term capital growth, simplicity and efficiency for future estate administration. A suitable cash buffer also needs to be maintained for medical, care and estate-related expenses. Given Alice has already exhausted her lifetime cap on means tested care fees and her primary place of residence prior to entry is about to be rented there is no requirement for any additional income. This is due to the net rent covering the aged care fees In reviewing Alice’s position, we have also reviewed Alice’s existing Macquarie Pension and are recommending a replacement platform that offers greater investment flexibility and stability. Overall, the advice will outline how to invest the lump sum appropriately, manage taxation considerations (including rental income), maintain a suitable cash reserve, and ensure Alice’s financial arrangements remain straightforward for you to manage under the Enduring Power of Attorney and eventually as part of her estate.

You are currently 79 and living in a care facility. You have appointed Rachael and Eric Moore as your enduring powers of attorney. You have approached us for advice on managing Alice's lump sum cash and to ensure that her financial arrangements are aligned with her long-term needs and estate intentions.

Show Alice as elderly lady sitting on a park bench. Then show a 50yo man and woman positioned either side of her. Then on bottom row, show large amount of notes on left and investment graph with two hands on right.

Scene Three – Scope And Goals

Invest surplus cash of $360,000 for long-term growth: Invest approx. $360,000 of surplus cash into a HUB24 Invest account structured with a Balanced or Growth strategy depending on the longer term cash requirements. The investment timeframe is greater than 5 years as Alice does not require these funds. The intention is that this capital will ultimately support or transfer to yourselves.

Maintain $50,000 cash buffer: Retain $50,000 in cash across high-interest and accessible facilities for contingencies such as medical needs, funeral costs, and estate administration.

Review existing Macquarie Pension with a more suitable platform: Review Alice’s current Macquarie Pension and consider another Platform due to ongoing concerns about Macquarie’s investment menu contraction, SMA/fund availability risks, and restricted manager access. Ensure continued access to diversified, high-quality growth options and stable portfolio administration.

Manage taxation efficiently in Alice’s personal name: Consider the impact of: •Rental income from Alice’s property •Pension income streams •Tax implications of retaining investments in her personal name •Preference for lower-income-generating, growth-oriented investments to manage taxable income

Ensure asset structuring supports smooth estate administration: Structure assets in a way that simplifies probate and enables flexibility for Rachael and Erik as attorneys. Consider whether assets may be wound down or transferred in specie at death depending on market conditions.

We therefore agreed that this advice will cover superannuation platforms and underlying investments. Your first goal is to invest surplus cash of $360,000 for a time horizon of more than 5 years, the intention being that this capital will ultimately transfer to Rachael and Eric.Your second goal is to maintain a $50,000 cash reserve in a high-interest and accessible facility for things like medical needs, funeral costs and estate administration. Your third goal is to review your existing Macquarie Pension due to ongoing concerns about investment menu contraction, fund availability risk and restricted manager access. Your last two goals are to manage taxation efficiently in your personal name, and to ensure asset structuring support smooth estate administration.

Scope:

1. Superannuation (platform)

2. Superannuation (investments)

Goals:

1. Invest $360k for 5+ years

2. Maintain $50k cash reserve

3. Review Macquarie Pension

4. Manage tax efficiently

5. Ensure smooth estate administration

Scene Four – The Advice

Advice 1: Replace Macquarie Pension Manager II with HUB24 Pension (Core)

•Macquarie’s SuperWrap platform has reduced and restricted investment manager access due to legal issues. Existing SMAs and underlying managed funds with Macquarie face potential future removal or constraint, increasing administration complexity and potential forced investment changes. •HUB24 provides: oBroader investment menus (existing SMA’s are available on HUB24) oGreater flexibility oCompetitive, aggregated fee structure across pension + investment accounts oSuperior long-term platform stability. •Continue minimum pension payments (currently $1,276.67/mth or $15,320 pa) •Ensures continuity of a conservative investment approach consistent with current Risk profile.

•Market volatility in growth assets. •Implementation timing risk: markets may rise or fall during transition.

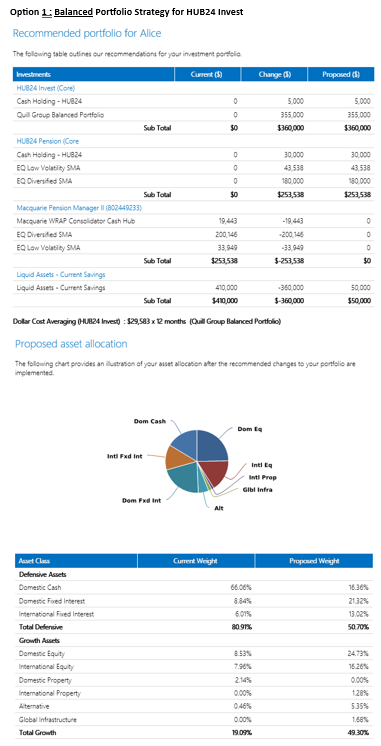

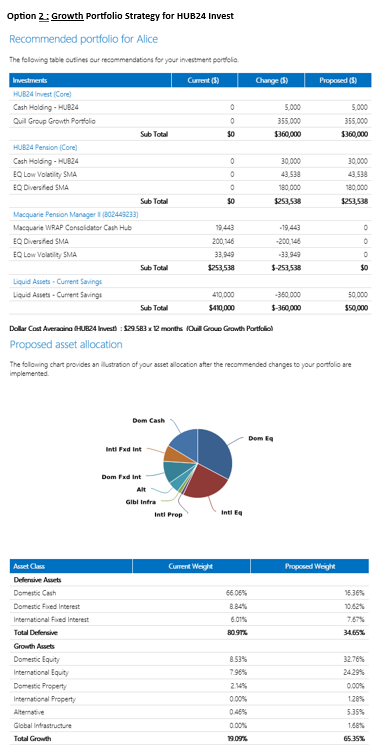

Advice 2: Invest $360,000 in HUB24 Invest Account (2 Options)

Option 1 : Balanced Portfolio Strategy

Option 2 : Growth Portfolio Strategy

•Alice does not require income from this portfolio; therefore, investment in longer-term capital growth options benefit the estate. •Growth-tilted investment aligns with the family’s view that funds will eventually pass to Judith, Rachael & Erik. •We’re providing 2 options for your consideration, dependent on expected timeframe of investment and possibility of cash required (Growth portfolio = longer timeframe). •Investing via Alice’s personal name is required as she is over the age of 75 and restricted from making super contributions. •A growth-tilted portfolio reduces taxable income, which helps manage taxation given rental income already contributes to her assessable income. •HUB24 Invest provides high-flexibility administration and investment options. •Invest funds via Dollar Cost Averaging over 12 months.

•Growth asset volatility may cause short-term declines. •Taxable capital gains may occur upon future sale of assets by executors. •Portfolio income returns are fully taxed at individual rates. •A beneficiary-focused strategy means higher growth exposure; you both must remain confident this aligns with Alice’s best interests.

Retain $50,000 Cash Buffer / Invest in Higher interest options

•Provides liquidity for unexpected medical expenses, care facility changes, funeral arrangements, estate legal fees or delays around probate. •Reduces the risk of forced sale of investments at an unfavourable market time. •Supports the financial management responsibilities as attorneys.

•Cash may not keep pace with inflation. •Low returns relative to growth assets.

Tax & Estate Structuring Strategy

•Rental income from the apartment will increase Alice’s taxable income; therefore growth-focused investing reduces taxable distributions compared to income-heavy assets. •Keeping assets in Alice’s name is more tax-efficient than distributing early to adult children, who are likely on higher marginal tax rates. •Investment structuring should remain simple so that probate is easily managed at death. •Provides flexibility for executors to transfer assets in specie, particularly if markets are depressed at the time of estate administration.

•Capital gains tax may apply depending on market timing. •Probate delays may temporarily restrict access to accounts. •If in-specie transfer is chosen, beneficiaries inherit cost bases and taxation liabilities.

My first advice is to replace your existing Macquarie Pension Manager with a new HUB24 Pension Core platform, continue your current minimum pension payment of $1,277 per month, and retain the investments within the platform as follows. Doing so will result in broader investment menus to facilitate long term growth at a competitive aggregated fee structure. Please be aware however that there will always be a degree of market volatility when investing in growth assets, and the markets may rise or fall during your transition from one platform to the other.

My second advice is to invest the $360,000 that you hold in your bank into a new HUB24 Investment Account and then investment the funds in one of the following two ways: either a growth portfolio strategy or a balanced portfolio strategy. Please note that investing in your personal name is required as you are over 75 and restricted from making super contributions. So you can make an informed decision, please note that investing in a growth portfolio offers longer term capital growth, is aligned with your family views that the funds will eventually pass to Judith, Rachael and Erik, and reduces taxable income. However, a growth portfolio is generally also more volatile, resulting in short term fluctuations. There may also be taxable capital gains upon future sale of the assets by the executors.

My third advice is to retain $50,000 as a cash buffer. Doing so will provide liquidity for unexpected medical expenses, care facility changes, funeral arrangements and estate management fees, while reducing the risk of forced sale of investments at unfavourable market times. However, please note that cash may not keep pace with inflation and suffer from low returns relative to growth assets.

In summary, please see the following benefits and risks of following my tax and estate structuring strategic advice.

Scene Five – Fees And Costs

Product fees

option-1-balanced-portfolio-and-aa.png

{kind=link}

option-2-growth-portfolio-and-aa.png

{kind=link}

replacement-of-product-costs.png

{kind=link}

Let's discuss fees.

The first is a one-off advice fee of two thousand two hundred dollars including GST, which covers the research and formulation of this advice.

The second is an ongoing service fee. Your current ongoing service fee is $2,652 per annum, which will be increasing to $4,290 per annum due to the higher amount of invested funds. This ongoing service fee places you on our Essentials Package, which means you will receive the following services.

Lastly, please note the following table which outlines the ongoing product costs that you will be paying to HUB24, and how it compares to your existing Macquarie platform on a like-for-like basis.

Same as previous videos with "Essentials" package. Please use third screenshot for the final fee product costs.

Scene Six – Disclosures

We have now covered the advice in full and with that, there are a few important points I need to make.

This Statement of Advice is for your consideration and your use only.

We have based this advice on information gathered from our discussions, and your completed Client Confidential Data Collection Booklet. We have assumed that this information is correct. Should any information have changed or be incorrect, you should contact us so we can review these strategies.

For information regarding benefits, interest and associations, please refer to the Financial Services Guide. We have already provided a copy, however you can view the latest version on our website. Alternatively we can e-mail or post a copy to you on request.

After you acquire certain financial products, a 14 or 28 day cooling off period will apply in certain circumstances. This means you can cancel or transfer to another financial product within this period if you decide this financial product no longer meets your needs. Please refer to the relevant product disclosure statement for details regarding your cooling off rights.

Finally, my advice remains current for a period of 30 days from the date of this video. If you decide to implement our recommendations after this time, or if your circumstances change during this time, please contact me so we can confirm that the advice continues to be suitable for you.

This advice purely considers your interests only, and is in your best interests. Please sign the authority to proceed if you wish to proceed with my advice. Otherwise, if you have any questions, please let me know. Thank you!

1. This SoA is for you only.

2. Let us know of any incomplete or inaccurate information immediately.

3. While we do not share any association with any of the products we have recommended in this advice, please refer to our FSG for further disclosures on any broad associations we may have.

4. 14-28 day cooling off period - please check relevant PDS

5. This advice is valid for 30 days from today's date.

Rest of scene is same as other final scenes